In Summary

- Medical insurance works by pooling premiums from many people to cover the costs of healthcare services from providers like psychiatrists and counselors, with the goal of averaging out expenses among all customers. Your insurance company ultimately determines the payment amount for your in-network provider’s services, not the provider themselves.

- You may receive a bill because insurance companies require patients to share the financial responsibility for care through a copay (set fee), co-insurance (percentage of the bill), or a deductible (annual amount paid before the insurance begins to pay). This cost-sharing encourages patients to consider the necessity of the medical services they receive.

Although the vast majority of people have medical insurance and the federal government even requires us to now have it, a great many people know little or nothing about how it works. For many people it is like their microwave or washing machine. They know what buttons to push to make it run but couldn’t tell you anything about the inner workings of it.

How Does My Insurance Work?

Medical insurance is a pooling of money paid by millions of people through their insurance premiums intended to provide coverage for medical services like psychiatry and counseling. The premiums go to insurance companies like BCBS, United Healthcare, or Health Partners. When you go to the doctor, you provide them with your insurance card and the clinic then bills the insurance company for the services provided. The giant pools of money from premiums are used to pay providers for their services. Each year, some people use their insurance, and some don’t, and it is intended to average out so there is enough money to cover the medical bills of those accessing care. At the big picture level, this seems like a great system to help people get the care they need. You might be wondering then, “Why did I get a bill?”

Why Did My Insurance Not Cover My Doctors Appointment?

Over decades of time insurance has created changes in how medical bills are paid. They try to keep premiums lower and make sure people are invested in the care they receive by putting a portion of the cost of medical bills on to the customer. Insurance companies believe that if medical care was 100% free, everyone would go all the time for everything, which would be an unnecessary waste of medical services and money. Putting some financial responsibility on patients makes them stop and think about how serious things are and if they really need medical care. This financial responsibility comes under a few different terms.

- Copay: A copay is a set dollar amount that the patient must pay for every medical visit. It could be $20 or quite high, perhaps $80. The higher the copay, often the lower the insurance premium as the patient is paying a good portion of the medical bill with their copay. Copays are typically due at the time of service.

- Co-Insurance: Similar to a copay, co-insurance is a percentage of the medical bill that the patient will have to pay. It could be as low as 10% or upwards of 30-50%. Co-insurance is typically billed to the patient after the insurance company pays their percentage to the clinic.

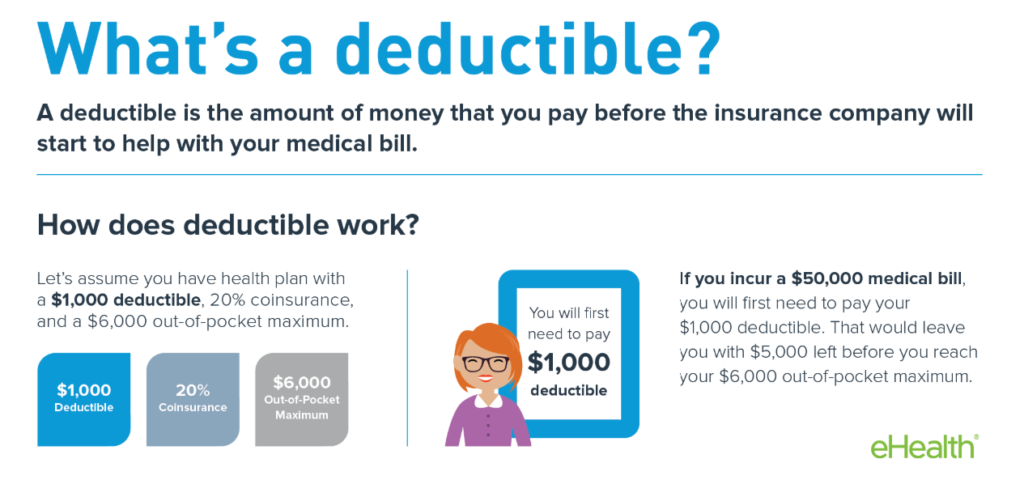

- Deductible: Each new year of the insurance plan, many people have to meet a deductible amount. This could be as low at $200 or as high as $3,000 to $10,000. What the deductible means is the patient is responsible for all medical expenses until the deductible amount has been reached. For a patient with a $200 deductible, this might be just one doctor’s visit. For those with high deductible plans, they may never hit their deductible even if they go to therapy weekly. Those with high deductible plans may not hit their deductible unless they were seriously injured and in the hospital for weeks.

Source: EHealthInsurance

Why is My Doctor Bill so High?

Most psychiatrists and therapists are credentialed and enrolled with each health insurance plan. This makes your provider “in-network”, which should get you a cheaper rate for the care. The providers who are on the insurance network have agreed to accept a payment amount for therapy and psychiatry appointments that is determined by the insurance company, not the provider. The reality is that your provider does not set the rate. Regardless of what they bill the insurance company, the insurance company only allows a certain rate for each service. Providers are not legally allowed to charge any more or less than what the insurance company has dictated. Many clients receive a bill from the provider because it has hit their deductible and mistakenly get frustrated with the provider thinking they are charging too much for the service, but it is important to remember that your provider did not pick this amount, your insurance company did.

We hope this information helps you understand the financial side of working with one of our psychiatrists or therapists. It may be important to call your insurance company to find out what your copay or deductible will be before you contact IPC to schedule an appointment. Please call us now at 763-416-4167, or request an appointment on our website: WWW.IPC-MN.COM so we can sit down with you and complete a thorough assessment and help you develop a plan of action that will work for you. Life is too short to be unhappy. Find the peace of mind you deserve.

To get more great resources, sign up for our newsletter, like us on Face Book, or follow us on Twitter.

Innovative Psychological Consultants

Peace of Mind You Deserve

Schedule An Appointment

"*" indicates required fields